Generali Global Assistance announces the results of 19th annual Holiday Barometer

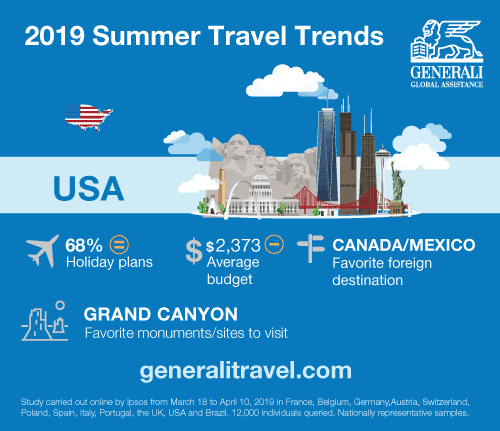

SAN DIEGO – June 4, 2019 – Generali Global Assistance (GGA) today announced the results of its 19th annual Holiday Barometer conducted on behalf of its parent company, Europ Assistance, by consumer research firm Ipsos. This year’s barometer found that the number of Americans who indicated that they would be taking vacation this summer held steady at 68 percent equal to the number of respondents in Brazil (68%) and five points higher than the number of European respondents (63%).

There were several interesting differences when it came to responses from Europeans, Americans, and Brazilians this year. US travelers indicated their travel budget for this year reduced by 10 percent to $2,373 (€2,131) while Europeans indicated that their travel budgets increased by 3 percent to € 2,019. The increase was mainly attributable to countries in the Euro Zone (which excludes the United Kingdom, Switzerland, and Poland) as budgets increased to €2,099 for that region. Brazilian travelers also indicated that their budgets decreased by almost 3 percent to R$ 5,058 (€1,138).

“In the 19th annual holiday barometer, we have seen the consolidation of many of the positive trends we have recognized in recent years,” said Chris Carnicelli, CEO of Generali Global Assistance. “While Americans have experienced a 10 percent reduction in their travel budgets, they are still the highest of those surveyed. As an assistance provider, we look to stay current with travel trends in order to accurately anticipate our customers’ needs. It’s part of our ‘you live we care’ motto that we look to fulfill every day.”

Americans are last in terms of how much vacation time they’ll take this year with respondents indicating 1.4 weeks on average. Interestingly, Brazil led all respondents at 2.2 weeks of vacation while Europe was close behind at an average of 1.8 weeks. Part of the 10 percent reduction in travel budget may have to do with where the majority of Americans plan on taking their vacation this year. While 35 percent haven’t decided on their destination yet, 50 percent of Americans indicated they would be traveling domestically this summer. In terms of destination type, American travelers were pretty closely split between beach (45%) and city (42%) destinations while Europeans (62%) and Brazilians (50%) preferred beach vacations.

One commonality was that budget was the most important factor when making plans to all European, American, and Brazilian travelers. Americans ranked taking part in leisure and cultural activities and the climate as their second and third biggest considerations, respectively. Risk of a personal attack and a terrorist attack rounded out Americans’ four and five spots, while comparatively Brazilians ranked them as their fourth and third biggest concerns. Europeans, on the other hand, ranked risk of terrorism as their fourth largest concern with risk of a personal attack coming in at number six. That said, the number of travelers who indicated they were concerned about terrorism was down across the board with percentages for Europeans, Americans, and Brazilians all dropping by six to seven points from years prior.

Americans are some of the most outdoorsy when it comes to atypical vacation activities with 46 percent indicating they would like to spend their summer vacation camping in the wilderness. That is compared to only 28 percent of Europeans who indicated they would do the same. Interestingly, Polish travelers had the highest number of respondents who indicated they would like to spend their vacation camping in the wilderness (52%). That said, Americans were also the most likely to work on their vacation with just 54 percent indicating they would be disconnecting completely – compared to the United Kingdom (76%), France (71%), Italy (67%), and Brazil (63%). Furthermore, 50 percent of US travelers indicated they would spend 30 minutes to 2 hours on work during their vacation time.

Methodology

The 2019 edition of the Cyber Barometer from Europ Assistance and Ipsos was conducted in 12 countries including the United States, United Kingdom, Italy, France, Spain, Switzerland, Germany, Austria, Portugal, Belgium, Poland, and Brazil. In each country, 1,000 consumers aged 18 years and older (aged 16 and up in Brazil) took part in an online questionnaire. The survey was conducted between March and April 2019 and investigated consumer holiday plans and travel preferences.

About Generali Global Assistance

Generali Global Assistance has been a leading provider of travel insurance and other assistance services for more than 25 years. The Company offers a full suite of innovative, vertically integrated travel insurance and emergency services, identity protection solutions, and beneficiary companion services. Generali Global Assistance is part of the Europ Assistance Group, the travel insurer and assistance provider of the multinational Generali Group, which for over 185 years has created a presence in 60 countries with over 76,000 employees. Our success has been built on the foundation of trust that clients have placed in our ability to provide assistance in the most difficult of circumstances.

Media Contact

Jesse Tron

M Group Strategic Communications (for Generali Global Assistance North America)

+1 646-417-8516

jtron@mgroupsc.com

www.generalitravelinsurance.com/press

Twitter: www.twitter.com/GeneraliTravel

Facebook: www.facebook.com/generalitravelinsurance/

Instagram: www.instagram.com/generalitravel/

Travel insurance plans are administered by Customized Services Administrators, Inc., CA Lic. No. 821931, located in San Diego, CA and doing business as Generali Global Assistance and Insurance Services. Plans are available to residents of the U.S. but may not be available in all jurisdictions. Benefits and services are described on a general basis; certain conditions and exclusions apply. Travel Retailers may not be licensed to sell insurance, in all states, and are not authorized to answer technical questions about the benefits, exclusions, and conditions of this insurance and cannot evaluate the adequacy of your existing insurance. This plan provides insurance coverage for your trip that applies only during the covered trip. You may have coverage from other sources that provides you with similar benefits but may be subject to different restrictions depending upon your other coverages. You may wish to compare the terms of this policy with your existing life, health, home and automobile policies. The purchase of this plan is not required in order to purchase any other travel product or service offered to you by your travel retailers. If you have any questions about your current coverage, call your insurer, insurance agent or broker. This notice provides general information on Generali Global Assistance’s products and services only. The information contained herein is not part of an insurance policy and may not be used to modify any insurance policy that might be issued. In the event the actual policy forms are inconsistent with any information provided herein, the language of the policy forms shall govern.

Travel insurance plans are underwritten by: Generali U.S. Branch, New York, NY; NAIC # 11231. Generali US Branch operates under the following names: Generali Assicurazioni Generali S.P.A. (U.S. Branch) in California, Assicurazioni Generali – U.S. Branch in Colorado, Generali U.S. Branch DBA The General Insurance Company of Trieste & Venice in Oregon, and The General Insurance Company of Trieste and Venice – U.S. Branch in Virginia. Generali US Branch is admitted or licensed to do business in all states and the District of Columbia.

Travel insurance plans are underwritten by: Generali U.S. Branch, New York, NY; NAIC # 11231. Generali US Branch operates under the following names: Generali Assicurazioni Generali S.P.A. (U.S. Branch) in California, Assicurazioni Generali – U.S. Branch in Colorado, Generali U.S. Branch DBA The General Insurance Company of Trieste & Venice in Oregon, and The General Insurance Company of Trieste and Venice – U.S. Branch in Virginia. Generali US Branch is admitted or licensed to do business in all states and the District of Columbia.

A7491905